¶ Emerita Resources Corporation

Market Cap: C$369 million

Share Price Range (52 weeks): C$0.46 – C$2.00

Free-Float: ~249 million shares

Volume (3-month avg): ~378k shares/day

Emerita was listed among the Top 50 TSX Venture Companies in 2025, highlighting investor confidence and growth trajectory

¶ Warrants

As of Q2 2025:

- Total Warrants Outstanding: 24,264,318

- These warrants form part of the fully diluted capital structure and may represent a potential source of future funding if exercised

¶ Options

- Stock Options Outstanding: 23,955,000

- Used primarily for executive compensation and employee incentives. Included in the total fully diluted share count of 311.86 million shares

¶ Financings

- Emerita has financed its operations primarily through equity raises. The March 2025 interim financials show:

- No new major financing events recorded in Q1 2025.

- However, a strategic approach has been to deploy funds into advancing the IBW project toward feasibility, as well as covering ongoing legal costs at Aznalcóllar.

¶ Loan

As of March 31, 2025:

Emerita Resources has an active convertible loan facility with Nebari Holdings, established in 2024. The total facility allows for up to CAD $15 million in funding, with CAD $6 million drawn as of the end of Q1 2025.

This facility represents the company's primary form of debt-based financing and is convertible, meaning Nebari may have the option to convert the loan into equity under certain conditions (though full conversion terms have not been publicly disclosed). The proceeds are being used to support exploration and development activities, primarily at the IBW project, and for general working capital.

While this loan introduces an element of leverage, Emerita remains relatively lightly geared compared to peers. Prior to 2024, the company had operated entirely on equity financing, meaning this marks a shift toward a more structured capital model as it moves closer to development readiness.

¶ Cash Runway

According to the interim results for the quarter ended March 31, 2025:

- Cash Position: C$10 million (approx.)

- Monthly Burn Rate: Historically ~C$1.5–2.0M/month at peak

- Estimated Runway: Approximately 3 to 4 months without further funding (depending on pace of PFS and legal spend)

- The company is not expected to require additional financing before Q3/Q4 2025 unless Aznalcóllar resolution or a JV occurs.

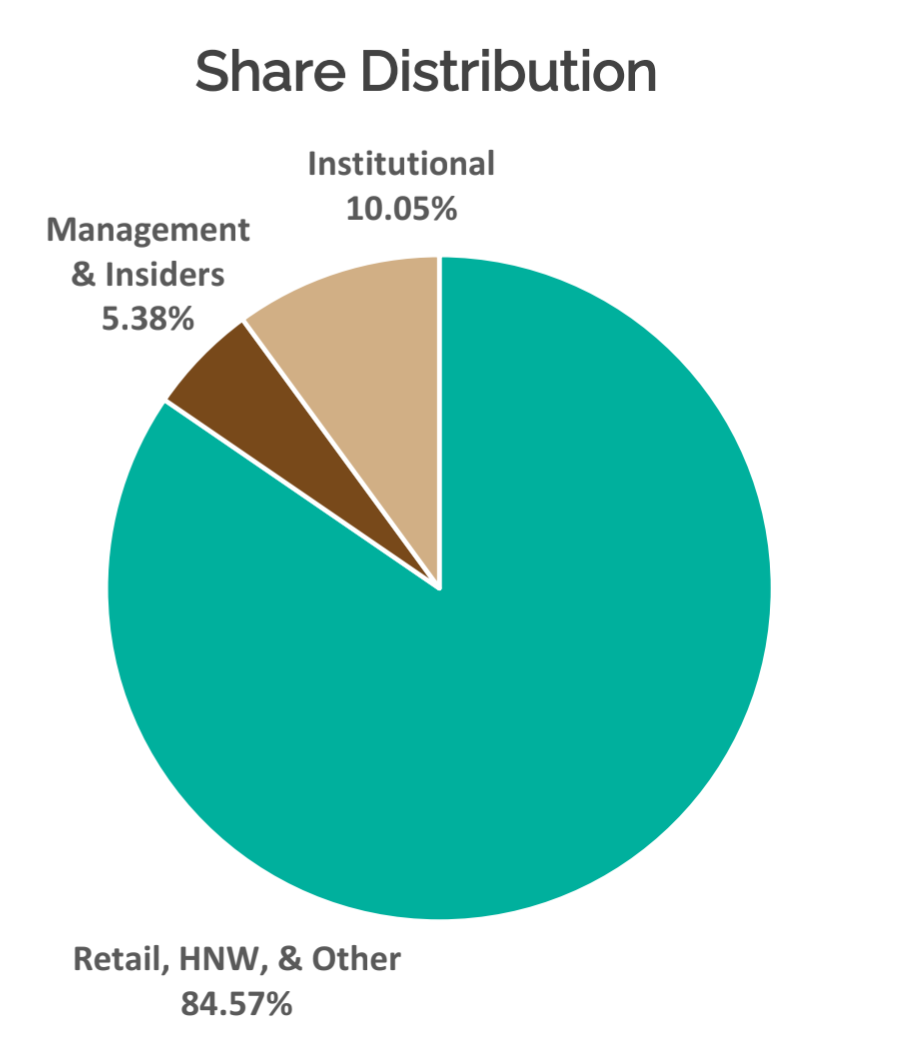

¶ Ownership

As of the most recent data:

- Retail, HNW, & Other: 84.6%

- Institutional: 10.1%

- Management & Insiders: 5.4%

This indicates a retail-heavy shareholder base, with strong support from private investors and limited institutional involvement to date — which could change rapidly on a positive Aznalcóllar resolution or IBW financing milestone

¶ Analyst Coverage - Summaries

¶ Canaccord Genuity - Dalton Baretto, CFA

Emerita Resources Corp. (EMO-TSXV) presents a compelling investment opportunity, as highlighted by Canaccord Genuity’s initiation of coverage on July 21, 2025, with a SPECULATIVE BUY rating and a 12-month target price of C$1.80 per share, implying an attractive 28% return based on a conservative 0.50x multiple of its fully risked Net Asset Value (NAV) as of July 1, 2025. Operating in Spain’s prolific Iberian Pyrite Belt, a world-class volcanogenic massive sulphide (VMS) district with over 5,000 years of mining history, Emerita’s flagship Iberian Belt West (IBW) project spans 7,667 hectares and boasts a robust March 2025 Mineral Resource Estimate of 26 million tonnes grading 13% ZnEq across three open deposits: La Romanera, El Cura, and La Infanta. The company’s early-stage Nuevo Tintillo property and its pursuit of the high-grade Aznalcóllar project, conservatively valued at 30% of its US$1.327 billion NPV, further enhance its upside potential. The conservative NAV weighting of Aznalcóllar, which assumes only a 30% chance of securing the tender, underscores the report’s cautious approach, potentially understating the significant value if Emerita prevails in the legal proceedings by July 2025. With excellent infrastructure access, a strong precious metal by-product credit, and substantial exploration upside from the recently acquired Ontario property, Emerita is well-positioned for growth in a top-tier, mining-friendly EU jurisdiction.

The analyst report’s conservative assumptions amplify the investment’s appeal, as they leave room for substantial upside while acknowledging manageable risks. Emerita’s experienced management team, led by CEO David Gower and President Joaquin Merino-Marquez, brings decades of expertise, bolstering confidence in the company’s ability to advance IBW and capitalize on exploration opportunities across its portfolio. While risks such as reliance on the innovative CLEVR technology for metallurgical recoveries and the Aznalcóllar legal outcome are noted, the report’s cautious 30% NAV weighting for Aznalcóllar and conservative commodity price assumptions (e.g., Zn $1.25/lb, Cu $4.50/lb, Au $2,200/oz) suggest that positive developments could significantly exceed expectations. The IBW project’s strategic location near existing mines and infrastructure, coupled with its fast-tracked Exploitation Permit application, positions it for streamlined development. Furthermore, the report’s sensitivity analysis, indicating a 25% NAV increase with a 20% zinc price rise, highlights the potential for outsized returns in a favorable commodity market. For investors seeking high-potential zinc exposure with significant exploration and legal optionality, Emerita offers a uniquely attractive risk-reward profile, with the report’s conservative stance suggesting that actual outcomes could deliver even greater value.

¶ Triple S Investing – “Special Situations” Deep Dive (Nov 2024)

In November 2024, Triple S Investing (an independent Substack focusing on special situations) published a 7-page deep dive report on Emerita Resources, honing in on the Aznalcóllar corruption case and its investment implications. Authored under the handle “Triple S Investing – Special Situations” on November 11, 2024, the report is titled “Emerita Resources: A Deep Dive into Corruption at the Aznalcóllar Tender Process.”. This piece reads like an investigative analyst report, thoroughly referencing Spanish court documents and drawing out the timeline of events. The coverage theme is centered on legal risk and reward: it recounts how Emerita has been “fighting a drawn-out legal war” over Aznalcóllar, an asset with an estimated US$25 billion in-situ metal value, by alleging the 2015 tender was “corrupt and rigged”. The Triple S analysis dives into specifics of the corruption: it cites the Seville Provincial Court’s 2021 findings that Emerita’s evidence unveiled systemic bribery, influence peddling, and manipulation in the bidding process. For example, the report highlights that officials allegedly provided the rival bidder (Minorbis/Magtel) access to confidential bid documents and even changed tender criteria mid-process to favor that bidder – clear breaches of law. Such detailed legal exposition is rarely seen outside of institutional research, underscoring the depth of due diligence. The Triple S author also reminds readers that Emerita is no stranger to legal battles – notably, the company “won its IBW mining concessions in a similar tender tussle” (defeating a Trafigura subsidiary in 2020). This past win provides a measure of confidence that Emerita could replicate that success with Aznalcóllar. By late 2024, the stage was set: the criminal trial for the Aznalcóllar case was scheduled to commence on March 3, 2025, with 16 defendants facing charges. Triple S framed Emerita as a high-upside, event-driven play – a “David versus Goliath” scenario in the Spanish mining sector.

In terms of valuation modelling, Triple S Investing took a bold stance by explicitly forecasting share price outcomes based on the legal result. The author posits that “a price target of ~C$4.00 per share on the first conviction or plea deal seems reasonable,” given that such an initial legal win would strongly validate Emerita’s claims. Furthermore, “the value should be north of C$6.00 a share” if Emerita ultimately is awarded the Aznalcóllar project and moves into development. This implies a scenario-based NAV where even partial legal success unlocks substantial value (likely factoring in a large portion of Aznalcóllar’s 60+ Mt resource at some probability weighting). At the time of writing, Emerita’s stock was trading well under $1, so Triple S was essentially arguing for a multi-bagger upside on a positive legal outcome. The report’s conclusion, titled “Betting on Justice: Emerita’s Opportunity”, characterizes Emerita as an unconventional mining investment – “a legal battle, a bet on regulatory reform” – but one where the evidence of wrongdoing is strong and the timeline for resolution is finally in sight. Triple S acknowledged the risk (investors must have the stomach for courtroom uncertainty) but asserted that the “potential upside could be transformative” if a fair outcome is achieved. This independent analysis thus complements the brokerage research by providing an unabashed special-situation thesis: it doesn’t delve much into IBW’s geology or near-term drills, but rather treats Emerita as a distressed asset play where unlocking Aznalcóllar could yield outsized returns. The inclusion of specific price targets ($4 and $6) tied to legal milestones distinguishes this report – effectively giving a sum-of-parts valuation: IBW’s ongoing progress plus a risked Aznalcóllar win. In summary, Triple S Investing’s November 2024 report offered a highly credible, institution-style deep dive into the Aznalcóllar legal saga, reinforcing the view that Emerita’s story is not just exploration, but also litigation-driven. It provided an original valuation framework for that saga (with explicit upside targets), thereby enriching the landscape of Emerita coverage alongside Clarus, Research Capital, and Rockstone’s work.

¶ Clarus Securities – Varun Arora (Equity Research Analyst)

Clarus Securities initiated coverage on Emerita Resources in mid-2021, highlighting the company’s flagship Iberia Belt West (IBW) project and the potential windfall from the contested Aznalcóllar mine tender. In an August 2021 launch report, analyst Varun Arora described Emerita as a “tier-1 polymetallic developer” in a world-class VMS camp, noting that “the IBW project alone offers [a] significant value proposition and M&A appeal,” while “a big prize for Emerita will be the awarding of the Aznalcóllar [project] public tender”. After promising drill results at IBW (e.g. high-grade intercepts at La Infanta in late 2021), Clarus maintained its “Speculative Buy” rating and raised the 12-month price target to ~CA$4.50–5.00 per share, citing expanding resources and improving commodity prices. Arora’s research at the time emphasized IBW’s growth potential (projecting a 3–6× resource increase versus historic estimates) and regarded Aznalcóllar as pure upside optionality pending legal outcomes.

Clarus has continued providing institutional-grade coverage through 2024–2025, updating valuation models as new data emerged. In a March 17, 2025 research note, Arora reported that Emerita’s global IBW resource jumped 37% to 25.77 Mt grading ~8.5% ZnEq (recoveries-adjusted), with mineralization still open at depth and along strike at multiple deposits. Clarus maintained a “Speculative Buy” rating with a CA$3.15/share target price, which implied ~119% upside from the ~CA$1.44 market price. This target reflected a risk-adjusted NAV primarily for IBW’s polymetallic deposits, given that IBW permitting is advancing and a Preliminary Economic Assessment (PEA) is expected by late 2025. The coverage themes in Clarus’ recent reports include IBW’s robust resource growth (with particularly high-grade copper-gold zones at El Cura and Romanera), a “catalyst-rich” year ahead (environmental permit approvals, the IBW PEA, and an exploitation license by 2026), and the status of the Aznalcóllar litigation. Notably, Clarus flagged the Aznalcóllar court case (the criminal trial began in March 2025) as a potential “game-changer” – a binary catalyst that is not fully priced in, but which could add considerable NAV if Emerita is awarded the project. Overall, Clarus’s institutional research frames Emerita’s valuation as being driven by IBW’s development (on which the CA$3+ target is based), with Aznalcóllar as a free upside option should the legal outcome be favorable.

¶ Research Capital Corp – Adam Schatzker (Equity Analyst)

Another brokerage providing in-depth coverage on Emerita is Research Capital Corp. Analyst Adam Schatzker initiated coverage around mid-2021, focusing on Emerita’s base metal assets in Spain and the evolving legal situation. In a June 2021 initiation report (titled “New Iberian Pyrite Belt, Zinc-Focused Company”), Research Capital outlined Emerita’s upside in the Iberian Pyrite Belt and noted that Spanish court decisions appeared to favor Emerita in the Aznalcóllar tender dispute. By November 2021, after further legal progress, Research Capital expressed high conviction in Emerita’s case – estimating “at least an 80% probability” that Emerita would prevail in the court cases – and maintained a Speculative Buy rating. At that time, Schatzker’s target price was ~CA$3.25 per share, implying that his valuation already assigned significant weight to a successful Aznalcóllar outcome. The analysis underscored Emerita as an excellent vehicle for exposure to Spain’s promising zinc-rich deposits, with IBW drilling success and the legal resolution acting as dual catalysts. Indeed, a Research Capital note from August 2021 had raised Emerita’s target after the first IBW drill results, stating “upside remains as drilling continues on IBW and the Aznalcóllar dispute approaches conclusion". This indicates their modeling included scenario analysis for the legal outcome.

Throughout 2022, Research Capital continued to update its thesis as Emerita aggressively advanced IBW (peaking at 14 drill rigs on site). The brokerage kept a Speculative Buy and adjusted its 12-month target upward to ~CA$4.00 by mid-2022, when Emerita’s shares traded below $1.00. Schatzker highlighted that ongoing step-out and infill results at La Romanera and La Infanta could “exceed the historical resource”, projecting a potential IBW resource base of ~42–43 Mt (vs. ~12 Mt historic) with materially higher grades. By late 2022, amidst market volatility, Research Capital modestly trimmed its target (e.g. CA$3.75 in November 2022) but firmly reiterated Emerita’s “significant fundamental value” even as the Aznalcóllar trial loomed. Key themes in Research Capital’s reports included the legal risk assessment (with detailed tracking of court developments and the decision to sequence the administrative and criminal trials) and project economics: Schatzker’s valuation breakdown implied that IBW’s ongoing resource growth and eventual mine development underpinned most of the target price, while a successful Aznalcóllar award could add several dollars per share in upside. The financing outlook was also noted – for example, Emerita’s mid-2023 capital raise (~CA$11M) to fund exploration was seen as shoring up the balance sheet, though both brokers acknowledge that full mine construction would require a substantially larger financing or partner in the future. Overall, Research Capital’s coverage has provided an institutional NAV-based valuation, balancing IBW’s tangible progress against the binary legal outcome, and it consistently maintained a bullish stance given Emerita’s unique position of potentially controlling two major base-metal deposits in a favorable jurisdiction.

¶ Rockstone Research – Stephan Bogner (Sponsored Research Series)

Rockstone Research, led by analyst Stephan Bogner, has published a series of deep-dive reports on Emerita Resources since 2020. These reports are institutional-style in their depth of geology and legal analysis, though they are sponsored by the company (disclosures note that Rockstone’s parent, Zimtu Capital, is paid by Emerita and holds equity). Despite the sponsorship, the Rockstone reports provide valuable insights, often including historical data compilations, project modelling, and context on Spain’s mining framework. For instance, Bogner’s September 2020 report (titled “From Zero to Hero”) announced Emerita’s win of the Paymogo exploration tender (now part of IBW) – heralding it as securing a “best-in-class zinc project in Spain” with extensive high-grade VMS potential. As IBW drilling got underway, Rockstone’s coverage expanded to follow results and estimate growth scenarios for the key deposits La Infanta, Romanera, and El Cura. One report noted that Romanera’s historic resource (~34 Mt @ ~7% ZnEq) could potentially grow toward 40+ Mt with deeper drilling and modern geophysics, framing IBW as a project with “tremendous growth opportunities”. Indeed, Bogner personally conducted a site visit in late 2021 and observed that Emerita’s on-the-ground team was rapidly advancing IBW with multiple rigs, lending credence to the aggressive resource expansion timeline (this was in line with Clarus and Research Capital’s bullish resource expansion forecasts).

Rockstone’s February 10, 2021 report stands out for its comprehensive legal and asset analysis of the Aznalcóllar situation. Published just after Spanish media reported the Aznalcóllar case was proceeding to trial, Bogner’s piece “Emerita trades heavy volumes amid…Aznalcóllar…ruling” detailed the alleged corruption in the 2015 tender and its implications. He explained that under Spanish law, if a crime was committed in a public tender, the award is nullified and the project must be granted to the next qualified bidder – in this case, Emerita. The report compiled Spanish press coverage and court findings, emphasizing that numerous officials and business principals were indicted for prevarication (abuse of power) in the awarding of Aznalcóllar. Bogner also underscored the scale of the Aznalcóllar/Los Frailes deposit, which was historically estimated at ~71 million tonnes grading ~3.8% Zn, 2.2% Pb, 60–84 g/t Ag (plus a high-grade subset of ~20 Mt at ~6.7% Zn, 3.9% Pb with higher silver). This world-class resource, dormant since the late 1990s, was portrayed as the trophy Emerita could clinch through the courts. Rockstone noted that Emerita had already invested heavily in Aznalcóllar’s tender process – spending over $1 million on a full mine plan, environmental and water management studies (~10,000 pages of documentation) – which underlined the company’s serious commitment. To fund its efforts, Emerita had just brought on Eric Sprott as a strategic investor (a $3M placement) and closed an additional $5.17M financing in early 2021, leaving it well-capitalized to “fast-track the Aznalcóllar project towards feasibility”. Throughout 2021, subsequent Rockstone updates tracked legal “wins” for Emerita (such as favorable court rulings in May and July 2021) and the expansion of Emerita’s land package (e.g. the acquisition of the Nuevo Tintillo property, discussed in Report #6). In summary, Stephan Bogner’s Rockstone reports (2020–2022) provided a richly detailed narrative combining valuation scenarios (e.g. in-situ metal values, peer comparisons), legal risk assessment, and on-site observations. While he did not issue explicit target prices, the tone suggested that if IBW reaches an NI 43-101 resource on the order of 1+ billion lbs Zn Eq (which could imply an NPV in the US$1–1.5 billion range) and if Aznalcóllar is awarded, Emerita’s market capitalization (then sub-$50M in early 2021) had multi-fold upside. Indeed, Rockstone pointed out that Aznalcóllar must be “attractive, possibly lucrative” – on the order of US$25 billion in gross metal value – “if there were crimes associated with its tender”, reinforcing why Emerita’s pursuit is worthwhile. This sponsored research thus echoed many themes of the sell-side analysts, affirming the long-term mine development vision and transformational potential of a legal victory, while also noting Emerita’s interim financings and partnerships to de-risk that journey.

¶

Sources: The above summaries are based on reports and notes from Canaccord, Clarus Securities, Research Capital Corp, Rockstone Research, and Triple S Investing, as well as coverage highlights via Streetwise Reports and company disclosures. Each report provides a distinct perspective on Emerita Resources – from sell-side analysts’ price targets and NAV estimates to independent researchers’ legal analysis and scenario modelling – collectively painting a comprehensive picture of the company’s valuation drivers (IBW exploration success, Aznalcóllar litigation outcome, and funding milestones). The convergence of these sources suggests a consensus on Emerita’s high-risk, high-reward profile: substantial intrinsic value in the IBW project and even greater upside if the courts deliver a victory. The institutional-grade coverage thus equips investors with both the quantitative valuations (e.g. price targets ranging from ~$3 to $5+) and the qualitative insights (legal probabilities, development timelines, financing needs) necessary to evaluate Emerita Resources as a junior mining investment.

¶ Doc Jones Due Diligence Coverage

Part 4 https://ceo.ca/@Drjimjones/emerita-resources-part4what-is-17-billion-in-metal-really-worth

Part 5 https://ceo.ca/@Drjimjones/400-million-ozs-of-silveremerita-resources-stuns-the-market-emo-part-5

Part 9 https://ceo.ca/@Drjimjones/victory-is-oursemerita-resources-emerges-as-a-titan-ddr-8

¶ Analyst Reports

Canaccord Genuity

July 2025 - Ole ore! Tapas, Toros and Tonnes in Spain PDF

Clarus

May 24, 2023 https://cdn-ceo-ca.s3.amazonaws.com/1i6s2o0-EMO-2023-05-24-Clarus.pdf (after 43-101 release)

August 4, 2022 https://cdn-ceo-ca.s3.amazonaws.com/1heova0-EMO-2022-08-04-Clarus.pdf

July 2021 https://cdn-ceo-ca.s3.amazonaws.com/1gflq5a-EMO-2021-07-23-Clarus-IR.pdf

September 2021 https://cdn-ceo-ca.s3.amazonaws.com/1gjjuup-EMO-2021-09-09-Clarus.pdf

November 16, 2021 https://cdn-ceo-ca.s3.amazonaws.com/1gp7c8s-Clarus%20update%20raises%20price%20target.pdf

November 30, 2021 https://cdn-ceo-ca.s3.amazonaws.com/1gtgbip-EMO-2021-11-30-Clarus.pdf

Research Capital

May 4, 2022 https://docdro.id/7yfGUWj

April 26, 2022 https://docdro.id/RzUdhyR

January 29, 2022 https://docdro.id/QdRMipj

Dec 2, 2021 https://cdn-ceo-ca.s3.amazonaws.com/1grpk43-29eb40019c86740a530084b0f1fb07ba.pdf

Rockstone

Update 22 Oct https://ceo.ca/@drjimjones?7bc513e3fd93

December 22, 2021 https://www.rockstone-research.com/index.php/en/research-reports/5940-Emerita-Site-Visit-Realization-of-Tremendous-Growth-Opportunities-with- High-Class-Projects-and-Technical-Team-in-Andalusia,-Spain

August 2021 https://drive.google.com/file/d/1JRxHJPtAgoHtZe5okDsYplwPcPAZb-h_/view?usp=sharing

PDFs